TMT sector

Huge deals mask downward trend in deal numbers

According to the latest data from global M&A information specialist Dealogic (part of the Ion Group), nearly 1,200 sponsor-backed deals involving European TMT businesses have been recorded since the beginning of 2021 – cumulatively worth a massive $182bn. However, the trend – at least in volume terms – has been downward, mirroring the overall global slump in M&A activity.

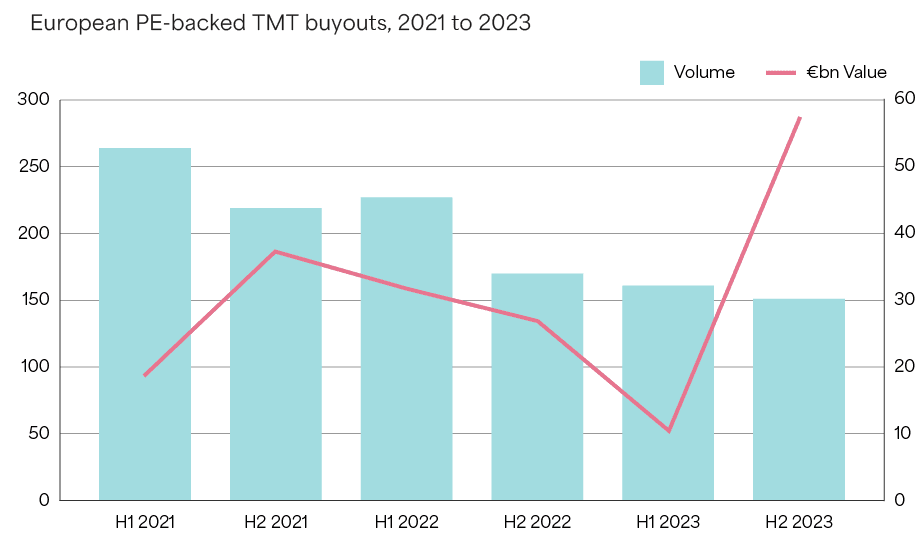

In half-yearly terms, M&A volumes were at their highest in the first six months of 2021, when 264 TMT deals were recorded, though that number fell by 17% in the second half of 2021 to 219. Despite rallying modestly in the first half of 2022, the ripple effects of the Ukraine crisis have taken hold, with deal volumes falling in three successive six-month periods; the second half of 2023 saw just 151 TMT deals, down 43% on H1 2021.

However, although the value of sponsor-backed M&A deals in the TMT space also followed the downward trajectory, from the $37.2bn seen in H2 2021 to $10.5bn in H1 2023, a sudden glut of huge transactions in the second half of last year saw the market reach a record $57.3bn. Two of these deals alone (both announced in November) accounted for $38.7bn including debt: the acquisition of FiberCop SpA in Italy by KKR and Abu Dhabi Investment Authority weighed in at more $23bn, while the buyout of Norway’s Adevinta by Permira, Blackstone and General Atlantic was worth $15.4bn.

Other notable transactions recorded by Dealogic in H2 2023 included the latest deal involving software giant Visma (HgCapital, ICG, TPG Capital, Amboise Partners et al), Civica Holdings (Blackstone) and Kahoot (Goldman Sachs, General Atlantic and Kirkby Invest).

It looks likely that growth in the TMT sector will be at best modest

Although broadly speaking there appears to be some confidence that M&A conditions will improve during 2024, it looks likely that growth in the TMT sector will be at best modest and the presence – or absence – of bulge-bracket deals will continue to drive the headlines.

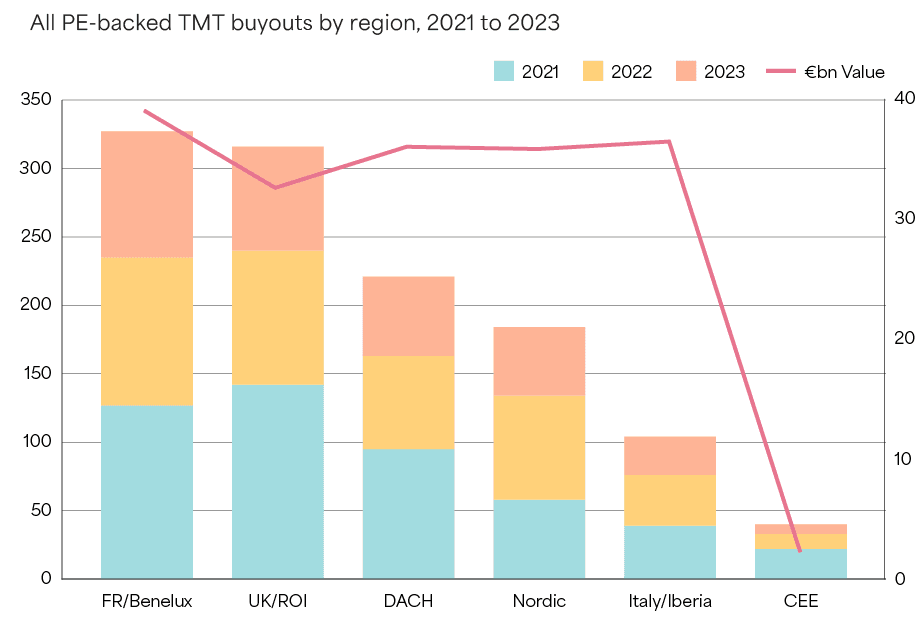

Looking at all TMT deals by region shows that France/Benelux and the UK are some way ahead of the other regions in volume terms. During the three-year period, they jointly added more than 640 TMT deals to the pot – 54% of the European total. The DACH and Nordic countries are next with 221 and 184 deals respectively, with Italy/Iberia recording just over 100 transactions.

However, the distorting effect of a handful of very large deals means that the value of TMT deals is shared much more evenly across Europe, with all regions except CEE generating TMT dealflow of $30-40bn during the timeframe. In the case of Italy/Iberia and the Nordics, much of that value came in the above-mentioned deals announced in late 2023. According to Real Deals’ data, other large transactions in the period include T-Mobile in the Netherlands (€5.1bn), Sophos in the UK ($3.9bn) and Circet in France (€3.25bn).

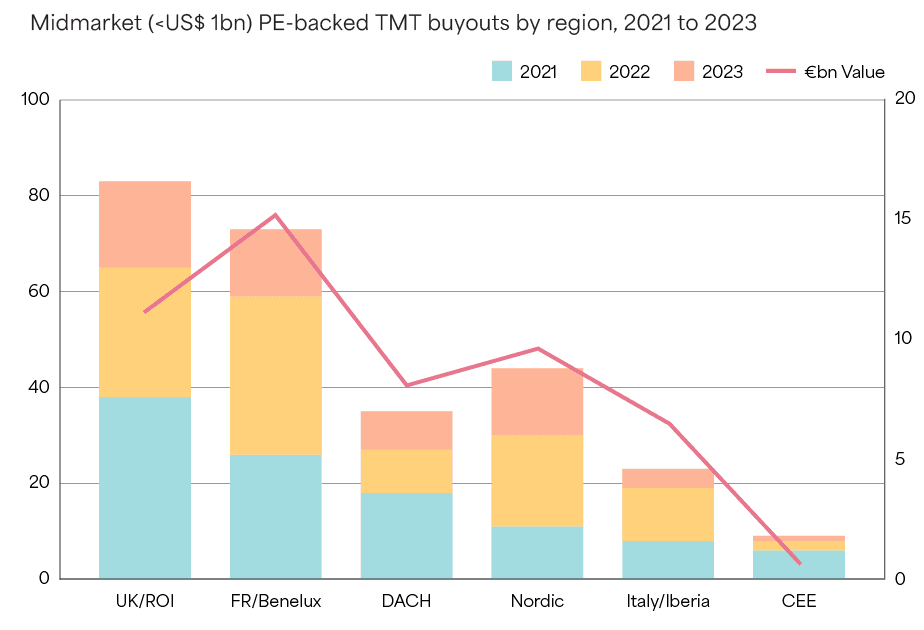

Looking at Dealogic’s midmarket subset (defined as those with a known value of less than $1bn) returns 267 transactions worth $51bn. However, the actual numbers are likely to be considerably higher in reality, as the data logged will not show transactions where no deal value was announced.

The regional dispersion of deals with a known sub-$1bn value shows a slightly altered regional pattern, with the UK comfortably ahead of France, and the Nordic countries outperforming the DACH region to rank third.

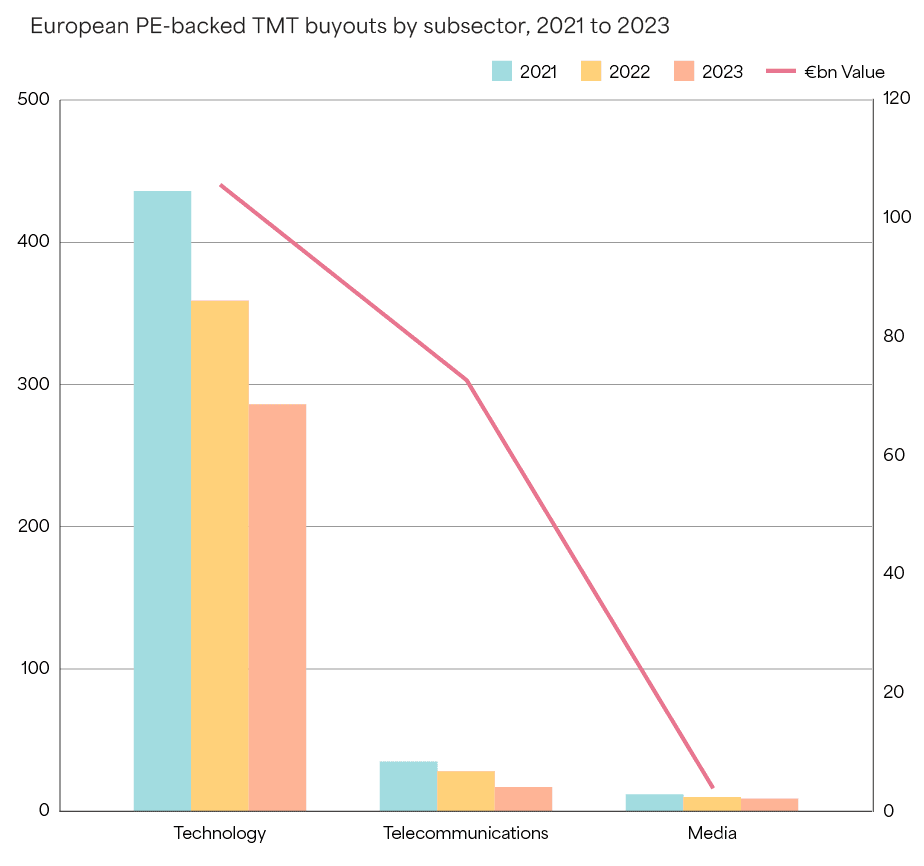

Broken into their main subsectors, Dealogic data clearly shows that TMT dealflow is dominated by deals in the tech space, which account for well over 1,000 (circa 91%) of the 1,192 deals recorded during the three-year period. The number of tech deals has fallen significantly, though, from the 436 seen in 2021 to 286 in 2023. The number of telecoms and media deals has also fallen (35 to 17 and 12 to nine, respectively) during the timeframe.

TMT dealflow is dominated by deals in the tech space

The dominance is not so significant in value terms, with very large telecoms deals boosting the total for that subsector to $72.7bn, compared with $105.6bn for the tech space. Media deals only contributed about $4bn to the total.

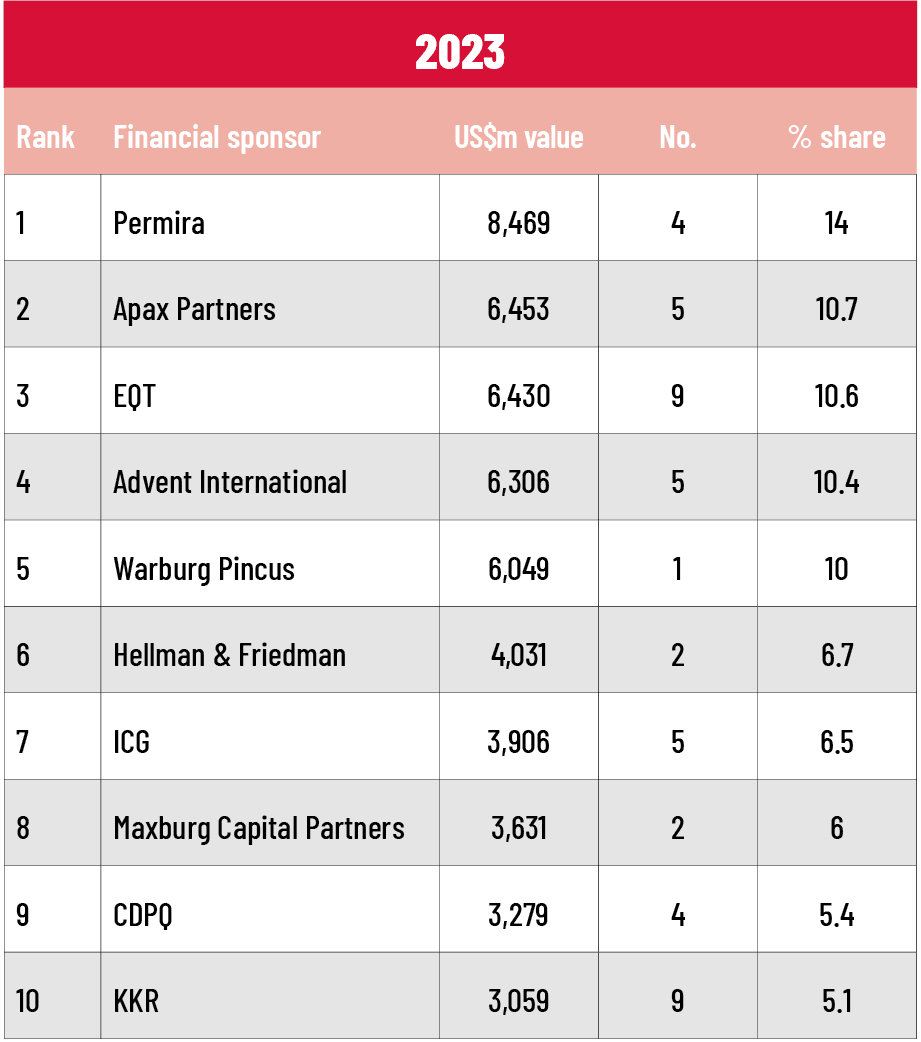

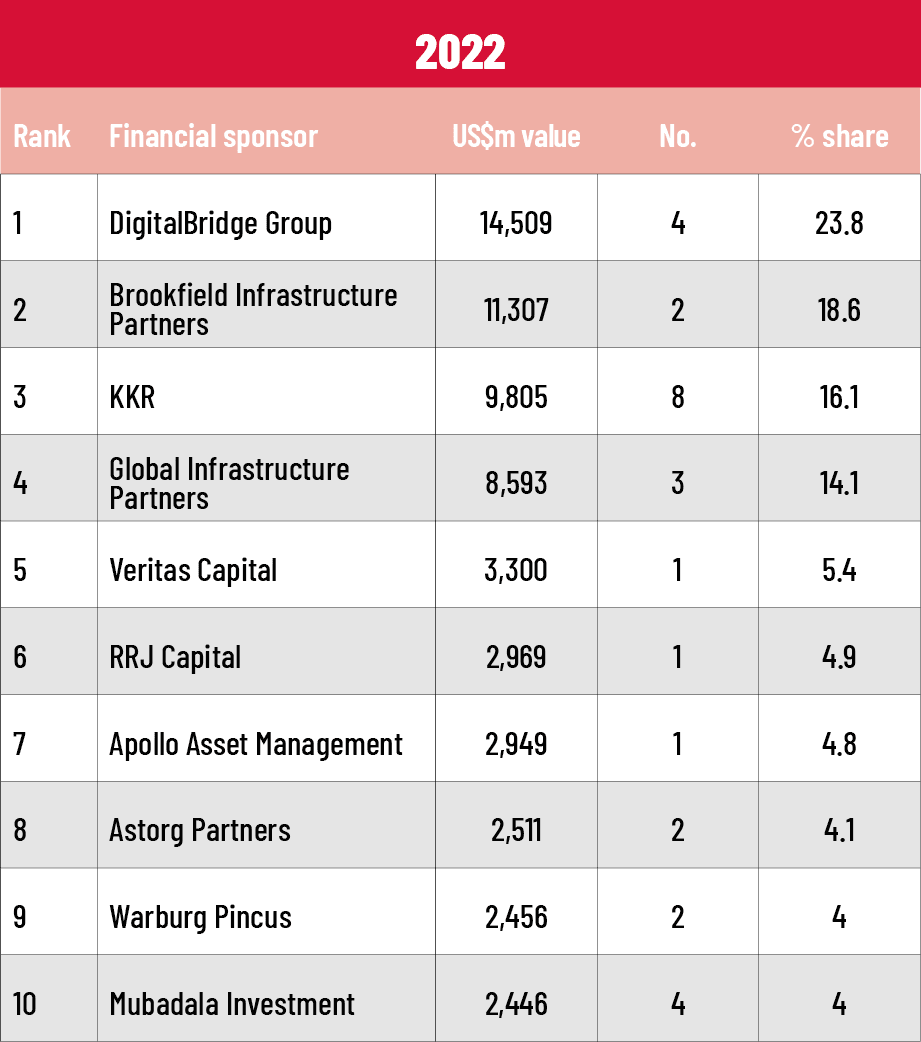

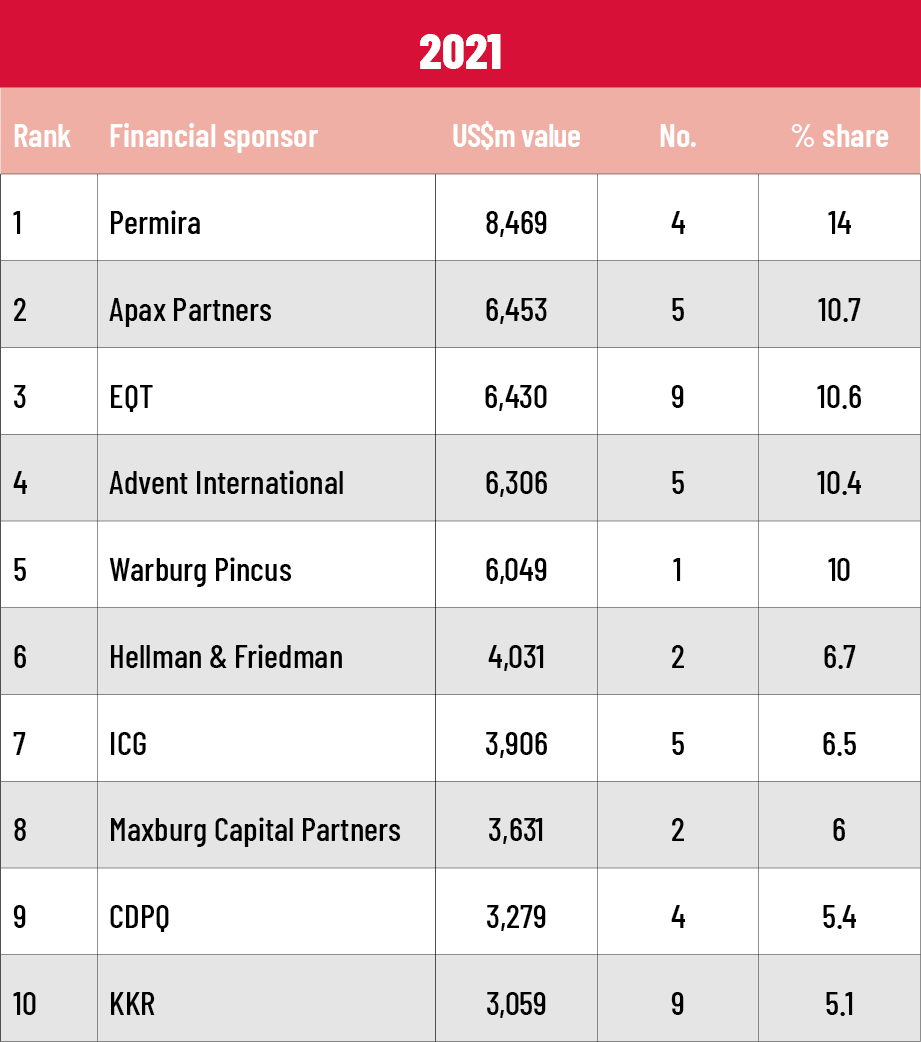

According to the latest Dealogic rankings, which are run based on announced deal values, the TMT space is unsurprisingly dominated by global PE and infrastructure giants active at the very top end of the market. In 2023 alone, no fewer than seven investors announced TMT deals worth more than $10bn in total. In among the annual top 10s by value are several European stalwarts such as Permira, Hg, Astorg, EQT and ICG.

Delving further into Dealogic data reveals a number of European midcap specialists that have been especially active during the three-year period. Dutch IT investor Main Capital, for instance, has announced no fewer than 43 TMT transactions in the timeframe – more than one a month. Others that would feature in a ranking by number of TMT deals include LDC (26), Hg, EQT and KKR (23 apiece) and Verdane (22).